Inventory Growth and Market Balance

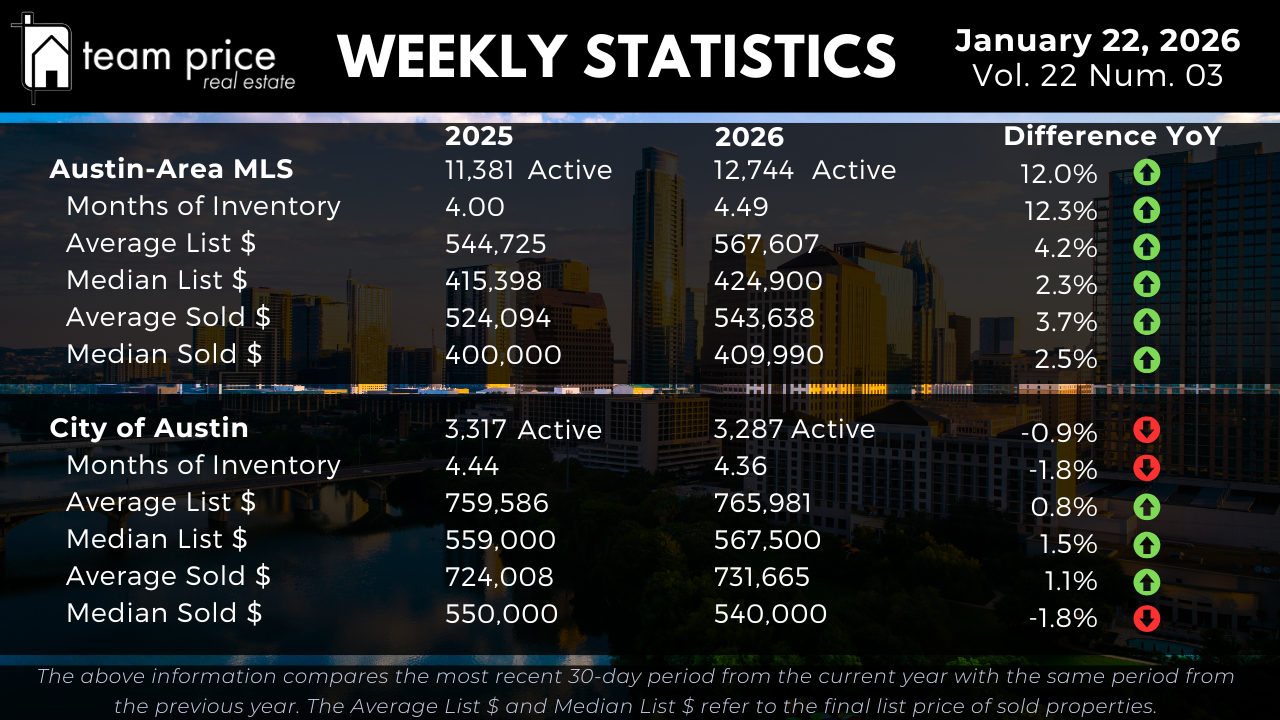

Active residential listings across the Austin-Area MLS total 12,744 this week, up from 11,381 at the same point last year, representing a 12.0% year-over-year increase in available supply. Inventory levels remain elevated, reinforcing that new listings continue to enter the market faster than homes are being absorbed through sales. Based on current transaction volume, Months of Inventory stands at 4.49, up from 4.00 last year, a 12.3% year-over-year increase and approximately a 1.1x expansion in supply relative to demand. This confirms a slower absorption environment than this time last year.

Inside the City of Austin, inventory trends diverge from the broader metro. Active listings declined modestly from 3,317 last year to 3,287 today, down 0.9% year over year. Months of Inventory also edged lower from 4.44 to 4.36, a 1.8% year-over-year decrease. Both metrics indicate relative stability rather than tightening, with sales velocity remaining slower than historical norms despite the lack of inventory growth.

Pricing Stability Across the MLS

Pricing across the Austin-Area MLS continues to show separation between average and median measures. The average active list price increased from $544,725 last year to $567,607 this week, a 4.2% year-over-year gain. Pricing at the average level remains supported by higher-priced inventory, while week-over-week movement remains limited.

The median active list price rose from $415,398 to $424,900, a 2.3% year-over-year increase, indicating modest price support in the middle of the market. On the sales side, the average sold price increased from $524,094 to $543,638, up 3.7% year over year. The median sold price rose from $400,000 to $409,990, a 2.5% year-over-year gain. Overall, sold pricing shows limited momentum, with higher-end closings continuing to influence averages more than medians.

Pricing Trends in the City of Austin

Within the City of Austin, pricing remains more constrained. The average active list price increased from $759,586 to $765,981, a 0.8% year-over-year gain. The median active list price rose from $559,000 to $567,500, up 1.5% year over year. These increases reflect stabilization rather than renewed appreciation.

On the sales side, the average sold price increased modestly from $724,008 to $731,665, a 1.1% year-over-year gain. In contrast, the median sold price declined from $550,000 to $540,000, down 1.8% year over year, indicating continued softness in mid-range transactions within the city.

Negotiation and Buyer Leverage

Negotiation remains prevalent across the Austin-Area MLS. So far this month, 72.30% of all closed sales sold below list price, up from 71.37% last month. An additional 18.39% sold at list price, while only 9.32% sold above list price, down from 10.55% last month and below January 2025 levels. The average sold-to-list price ratio currently stands at 96.58%, confirming that discounted pricing and seller concessions remain common.

Regional and ZIP Code Variations

Market performance continues to vary widely across Central Texas. Of the 30 cities tracked, 11 recorded month-over-month price increases, while 19 experienced declines. The same split holds year over year, with 11 cities posting gains and 19 posting declines. No cities are trading above their peak prices from the past 12 months, with 29 still below peak levels.

At the ZIP code level, dispersion remains pronounced. Among the 75 ZIP codes tracked, 32 recorded month-over-month price increases while 42 declined. Year over year, 31 ZIP codes showed price increases and 42 declined. None of the tracked ZIP codes are above their recent peak prices, with 73 still below peak levels.

Prices Relative to Peak Levels

Prices across the Austin-Area MLS remain materially below prior market highs. The average list price is down approximately 11.1% from its March 2023 peak, while the median list price is down about 21.3% from its May 2022 high. The average sold price is down roughly 15.1% from peak, and the median sold price is down approximately 22.8%. On a price-per-square-foot basis, average and median sold values remain roughly 24% to 27% below their 2022 highs.

Within the City of Austin, peak-to-current declines remain significant. The average list price is down approximately 9.5% from its September 2025 peak, while the median list price is down about 13.5% from its May 2022 high. The average sold price is down roughly 9.9% from peak, and the median sold price is down approximately 12.8%. On a price-per-square-foot basis, values remain roughly 22% to 28% below peak levels.

Market Outlook

As of mid-January 2026, the Austin housing market continues to operate in a slower, more balanced environment. Inventory across the Austin-Area MLS is higher, Months of Inventory remains elevated, and the majority of homes are selling below list price. Pricing support persists at the upper end of the market, while median pricing shows limited momentum, particularly within the City of Austin. The market remains defined by balance, measured demand, and price sensitivity rather than broad-based appreciation.